1 year ago

32

1 year ago

32

In March, we explored the difference between Home Equity Conversion Mortgage (HECM) “expected rates” and “note rates” and why most reverse mortgages depend on these two interest rates. In April, we specifically focused on expected rates. We showed that when expected rates increase and round up to the next 1/8% (0.125%), the principal available to a prospect is typically reduced by an average of 0.6% (of the home’s value).

In the month since my last rate update was published, expected rates increased 39 basis points (0.39%), which rounds to 3/8%, or 3 principal limit cuts. Sadly, these higher expected rates have reduced the initial funds available for new HECM applicants.

But could there be a silver lining to higher rates? Maybe. When short-term rates increase, existing HECM clients will see their borrowing capacity increase at a faster rate. This brings us to the second rate, the note rate.

What about note rates?

Therefore, it’s understandable why rising rates might cause concern for many borrowers. However, rate increases from month-to-month don’t impact the principal and interest payments of a reverse mortgage; those required monthly payments went away when the reverse mortgage was funded.

Interest charges simply accrue. If payments are not made, then the loan balance will rise.

So, what is the benefit of higher note rates?

Homeowners with sizeable loan balances generally want interest rates to go down, but borrowers who are willing and able to wait to draw funds will benefit from higher rates.

This is because the unused principal of a HECM adjustable-rate mortgage (ARM) will grow at the same rate that is applied to the loan balance.

For example, a HECM loan balance accruing interest at 7.50% (+0.50% in MIP) would have a line of credit (LOC) growing at an annual rate of 8%, compounding monthly at 1/12th of that rate.

The same is true of any unused proceeds like a Life Expectancy Set-Asides (LESA). In fact, repair set-asides and funds allocated for tenure and term payments will grow in the borrower’s favor as well, providing greater borrowing power in the future.

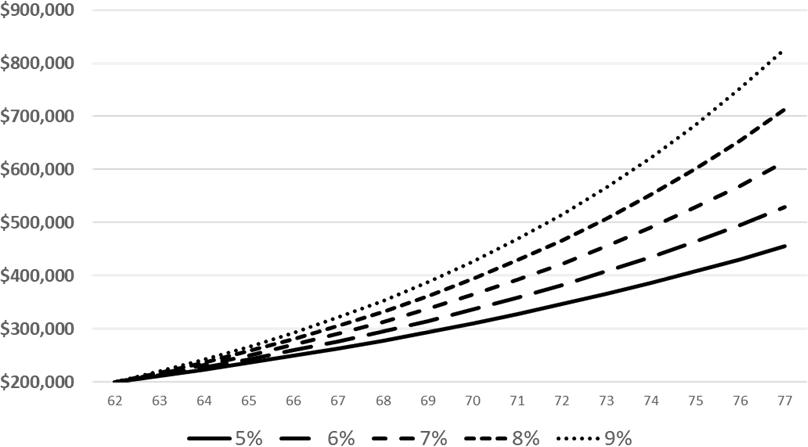

Example

Consider 62-year-old “Harry Homeowner” who has no existing mortgage. Harry wishes to utilize the HECM ARM line of credit and its growth for future cash flow needs. Harry establishes an initial line of credit of $200,000. The LOC and its growth can be modeled (below) to demonstrate the power of compounded growth at various rates.

- With a note rate of 5%, the LOC after 15 years would grow to $455,517.

- With a note rate of 9%, the LOC after 15 years would grow to $826,919.

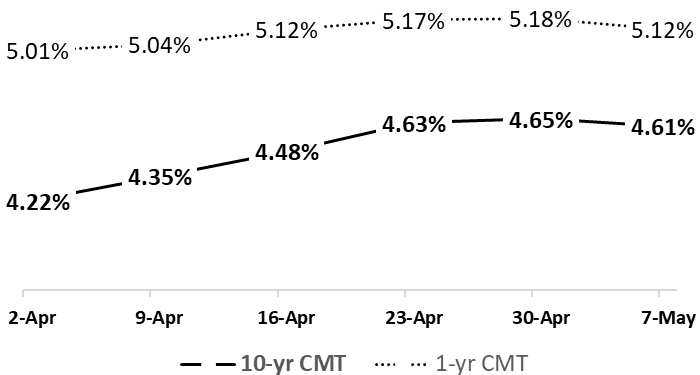

May 2024 update

The 10-year CMT weekly average (used for calculating expected rates) increased 39 bps over the last month. However, the trend is lower after last week’s jobs report.

The current weekly average 4.61% is added to the lender margin and in effect for loans originated May 7 through May 13. The spread between the average 10 year and 1-year CMT has narrowed as shown here:

This column does not necessarily reflect the opinion of Reverse Mortgage Daily and its owners.

To contact the author of this story: Dan Hultquist at [email protected]

To contact the editor responsible for this story: Chris Clow at [email protected]

English (US) ·

English (US) ·