In India,

foreign remittances

by individuals come under

RBI

's Liberalised Remittance Scheme (

LRS

) with individuals allowed to remit up to $250,000 annually without seeking prior approval. The scheme seeks to simplify and liberalise transfer of funds to meet a range of purposes, including education, travel, medical treatment, gifts to relatives and investments.

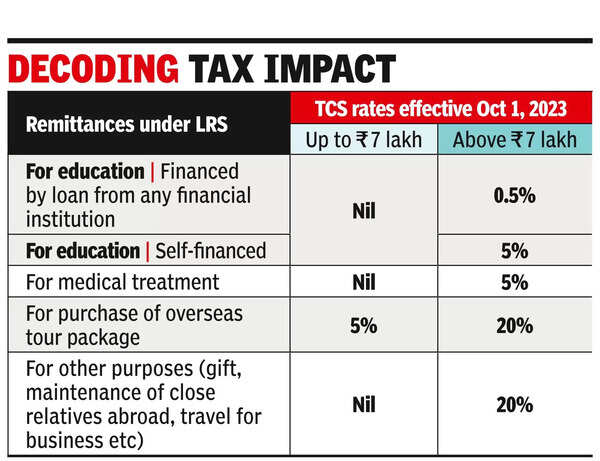

To track funds remitted, Tax Collection at Source (TCS) was introduced by the Finance Act, 2020.

TCS

was mandatory on remittances exceeding Rs 7 lakh and sale of overseas tour packages (without any monetary limit). Later, the TCS rates and thresholds on LRS on such remittances were modified with effect from Oct 1, 2023.

CBDT also clarified that expenditure incurred through international credit cards when an individual is overseas would not attract TCS until further notice. It is pertinent to note that there is no clarification regarding TCS not being applicable on transactions done using international debit cards overseas. Budget 2024 may provide clarity on TCS on expenditure incurred through such credit and debit cards.

The circular also provided clarification on the various kinds of expenses that could be considered part of education, medical treatment and overseas tour packages. The expenses for medical treatment include air-fare (including air-fare for attendant), accommodation and food, local transport, medical expenses incurred and day-to-day expenses. Further, the threshold of Rs 7 lakh is a combined threshold irrespective of the type of remittance.

Let's consider the case of Mr A who remits Rs 7 lakh in a financial year for his son's education and subsequently remits another Rs 5 lakh for investments abroad. The first remittance of Rs 7 lakh shall not be subject to TCS, however TCS shall apply for the subsequent remittance of Rs 5 lakh at applicable rates.

There are associated challenges with

TCS compliance

requirements, which revolve around financial and administrative issues. The need to pay TCS upfront and high TCS rates of 20% can result in significant additional cash outflow, impacting an individual's liquidity. While similar to tax deducted at source (TDS), TCS can be adjusted against one's income-tax liability, there is no clarity on whether the employer can consider TCS at the tax withholding stage. If the TCS paid exceeds the actual tax liability, individuals can claim a refund when filing their income tax returns. However, the refund process can be lengthy and may lead to financial inconvenience.

On the administrative front, compliance with TCS requires meticulous documentation and record-keeping, including providing PAN details, which can increase the workload for individuals. Most importantly, there may be lack of awareness and understanding of the new TCS regulations among individuals, leading to potential non-compliance.

As we approach Budget 2024, one will need to wait and watch whether any relaxations on TCS on LRS transactions are provided. Such relaxations will provide much-needed relief to individual taxpayers and facilitate smoother transactions for those remitting funds under LRS.

(The writer is partner, EY India; Rajesh Sureshan, director, EY India, also contributed to the article. The views expressed are personal)

English (US) ·

English (US) ·